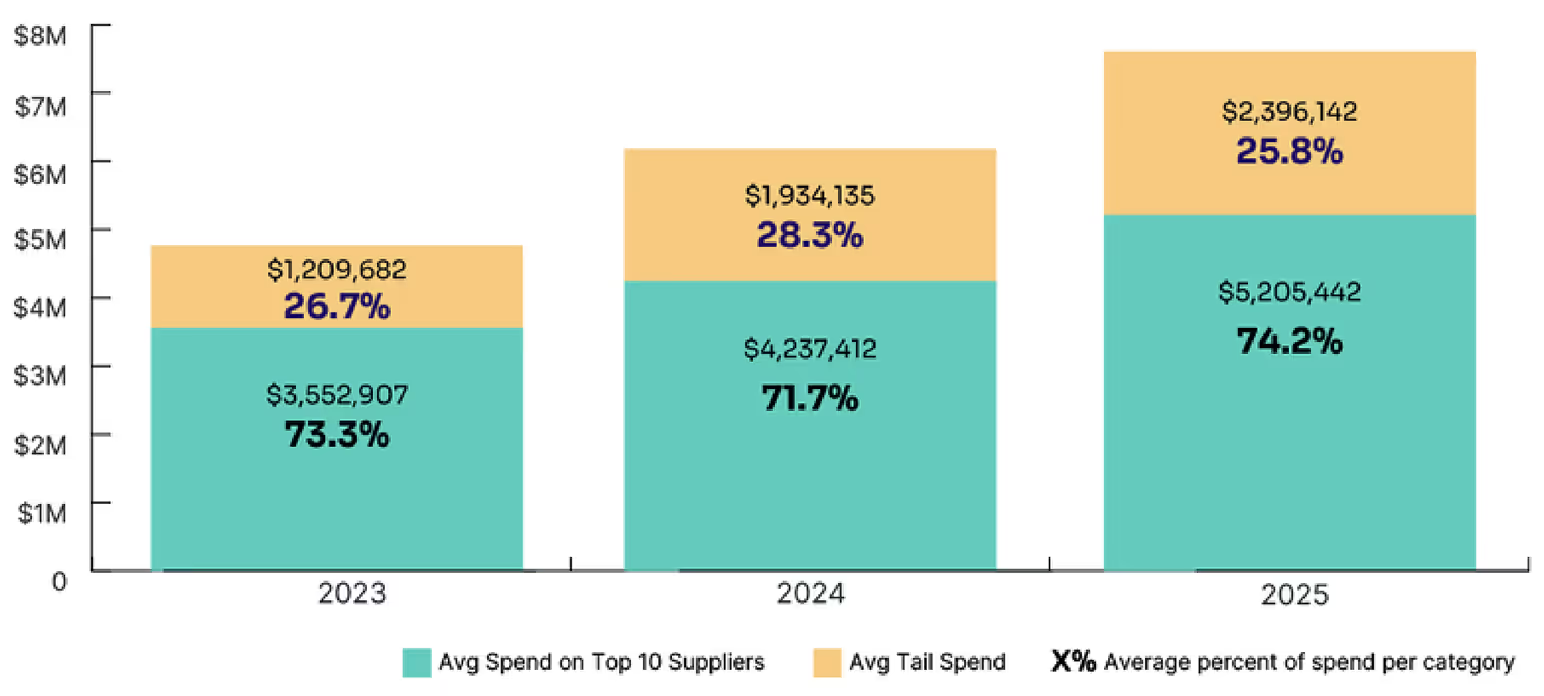

Top 10 vendors command 74.2% of total software spend - unchanged for three consecutive years despite AI proliferation - with absolute dollars increasing 46% from $3.55M to $5.21M while long tail shrank to 25.8%. Major platforms captured AI budgets through embedded features and 20-37% price increases. Effective SaaS budgeting tiers vendors by spend, initiates top-10 renewals 3-6 months early for 39% higher savings, audits overlap for consolidation leverage, and establishes AI guardrails before negotiations.

Pull up your software spend report right now. Sort by total contract value, descending.

Somewhere around the tenth row, something interesting happens: the numbers drop off a cliff.

What's above that line is where your largest financial exposures live. That's not to dismiss the tail - pricing variability data shows genuine savings opportunity there - but no amount of tail spend optimization changes the math when nearly three-quarters of your budget is concentrated in ten relationships.

Tropic's analysis of over $18B in spend under management confirms it: your top 10 vendors command 74.2% of average total software spend - a concentration that has held steady for three consecutive years, through a market correction, and the most aggressive wave of AI tool adoption in history.

The long tail got louder and managing AI proliferation is the right problem to work on right now, but don't let it pull focus from your top 10 vendors that comprise a strong majority of your software dollars.

What Three Years of SaaS Budgeting Data Shows

The spend concentration data from Tropic's 2026 Software Buying Trends Report is striking in its consistency. Here's what three years of data tells us:

- 2023: Top 10 suppliers = $3.55M average spend (73.3% of total budget)

- 2024: Top 10 suppliers = $4.24M average spend (71.7% of total budget)

- 2025: Top 10 suppliers = $5.21M average spend (74.2% of total budget)

That's a 46% increase in absolute dollars to your top vendors in just two years. And the tail - despite all the AI experimentation and tool proliferation - has actually shrunk as a share of overall spend, dropping from 28.3% in 2024 to 25.8% in 2025.

Let that sit for a moment. We're in what many are calling the golden age of AI tool adoption. New vendors. New use cases. More line items on the SaaS budget than ever. And yet concentration is getting more pronounced, not less.

Why? Because the biggest vendors are capturing AI budget too. Microsoft, Google, and Salesforce aren't losing wallet share to AI-native challengers; they're acquiring them, embedding AI features into existing contracts, and raising prices to reflect it. The AI Tax is very real, and your top 10 vendors are the ones applying it most aggressively.

Your SaaS Budgeting Blind Spot

Spend concentration creates a specific kind of organizational blind spot.

Most procurement and finance teams have built their workflows around volume of vendors: intake processes, approval workflows, budget thresholds, vendor review cadences. The implicit logic is that more vendors mean more risk and more work. Spread attention accordingly.

But we can forget that spend concentrates. And when your top 10 or so relationships represent nearly three-quarters of your software spend, an underinvested relationship there is categorically more expensive than a mismanaged one in the tail.

Think about the mechanics. Getting a 20% discount on a $300K HubSpot renewal is $60,000 back in the budget - real enough to fund a hire, offset a price increase elsewhere, or improve margin by a measurable basis point. Getting 20% off a $15K tool nobody's fully adopted yet is a $3,000 win that takes the same calendar time to close. Only one of them really compounds.

How to Manage Your Top 10 Vendors Like the SaaS Budget Line Items They Are

There's a difference between a vendor you spend a lot with and a vendor you manage strategically. Fewer do the latter. Here's what the distinction looks like in practice:

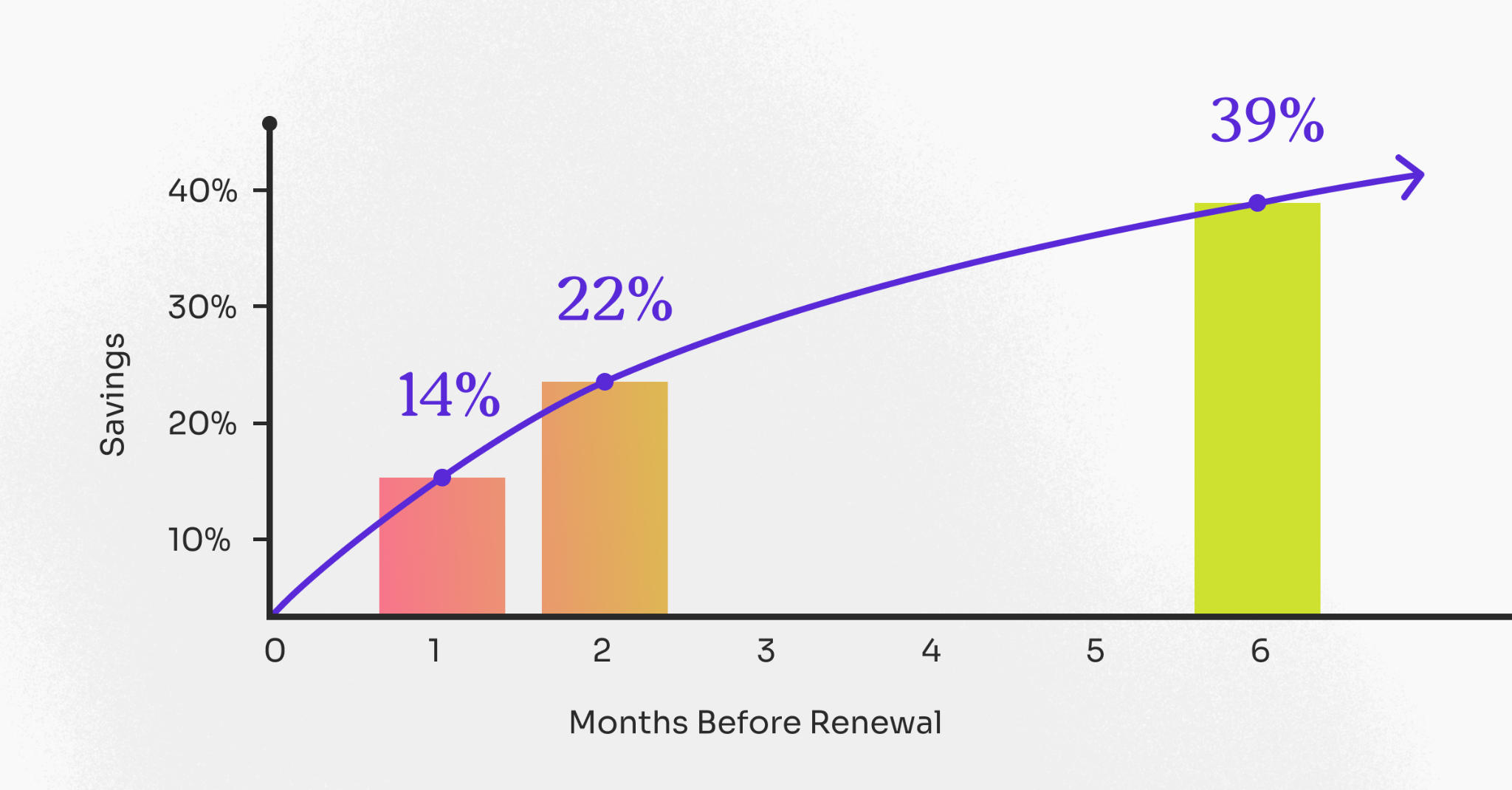

1. Renewal isn't the only touchpoint: For all your renewals, especially your top-10 vendor relationships, waiting for renewal to engage with them is already too late. Strategic vendor management requires quarterly business reviews, mid-year commercial check-ins, and continuous usage monitoring. You should know your consumption trends and adoption rates. According to our data, the earlier you engage, the more money you’re able to save.

2. You've mapped the full commercial envelope: Price is one variable, but your top vendors are also the ones most likely to have auto-renewal clauses, unpredictable true-up mechanisms, seat ratchets, and AI add-on upsell language embedded in the fine print. Spend variance data shows that the same vendors dominating your SaaS budget are also the ones driving the biggest gaps between contracted amounts and actual spend. Vendor relationships at this tier require ongoing contract monitoring, not just point-in-time review.

3. Consolidation is a lever, not just a cleanup exercise: If Microsoft, Google, and Salesforce are all in your top 10 - and they likely are - you almost certainly have overlapping capabilities across those contracts you're not exploiting. Unified communication. Productivity suites. CRM and marketing automation. Each of those vendors wants more of your wallet, which means each of them has an incentive to offer bundle discounts if you bring a consolidation proposal to the table. That's software cost optimization at scale (which most companies leave unused).

4. You know your walk-away position before you sit down: Concentrated spend creates more dependency on these select few vendors. When Salesforce or Workday represents 15% of your software budget, the implicit assumption in every negotiation is that you're not going anywhere. Don’t listen to that assumption. You’d be surprised. Benchmark your current pricing against market data, identify viable alternatives, and make sure your vendor knows you've done both.

The Long Tail Still Has a Role in Your SaaS Budget

I don’t want readers to think that the long tail is the enemy. It isn’t. And experimentation on new tools is healthy. The AI tools showing up as fastest-growing in spend - Cursor at 4,300% YoY, Anthropic at 1,900% - started in the tail. Killing new tool adoption in the name of consolidation is its own form of operational risk.

The right way to frame this isn't spend less in the tail. It's more like graduate tail vendors intentionally.

Define what "graduation" looks like for your organization before a tool gets there.

- At what spend threshold does a vendor move from ad hoc to managed?

- What's the process for onboarding them into formal procurement workflows?

- Who owns that relationship once it's more strategic?

Without clear criteria, tail vendors drift upward in spend without the oversight that should accompany the growth. One day you're approving a $20K pilot. Two years later, it's a $120K dependency you don't have a playbook for. That's how SaaS sprawl quietly reshapes your budget without anyone signing off on it.

Practical SaaS Budgeting Roadmap Built Around Spend Concentration

If you're looking to reorient your procurement and budgeting model around these realities, here's where to start:

- Tier your vendor portfolio by spend, not by category: Your top 10 by dollars deserve Tier 1 treatment: dedicated relationship ownership, quarterly reviews, board-level visibility on renewal timing, and proactive benchmarking. Tier 2 (the next 10-20 vendors) gets structured renewal management. Everything below that gets governed through automated alerts and defined approval thresholds. While this is a more generalized structure, customize your tiers to what best fits the needs of your organization and CFO.

- Build a renewal calendar 12 months out, minimum: Your top 10 vendors should have renewal conversations initiated no later than 3-6 months in advance (depending on vendor). Time is procurement's most undervalued currency.

- Audit for hidden overlap in your top 10 now: Pull your full contract list across your largest vendors and map feature overlap. Where are you paying for capabilities twice? Where does one vendor's enterprise tier eliminate the need for a point solution in the tail? This is all about building a consolidation narrative that gives you negotiating leverage with the vendors you're consolidating toward.

- Assign ownership, not just visibility: Concentrated spend requires accountable ownership. Every top-10 vendor relationship should have a named owner responsible for commercial performance, usage monitoring, and renewal strategy, not just a category manager who gets looped in 60 days before contract expiration.

- Set AI spend guardrails before you need them. Your top 10 vendors are repricing for AI aggressively. The average AI-driven price uplift at renewal is 20-37%, compared to the 3-9% historical norm. If Microsoft, Google, or Salesforce is in your top 10, assume they're coming to your next renewal with AI add-ons, forced SKU migrations, or bundled packages that obscure unit economics. Get ahead of it: document which AI features you're actually using, establish ROI thresholds before renewal conversations start, and treat AI pricing as a negotiation variable rather than a fixed cost.

Don't Forget Your Top 10

Nobody is saying ignore the tail. You should govern it, experiment in it, and graduate vendors out of it deliberately.

But the data has been consistent for three years: your top 10 vendors own nearly three-quarters of your software budget. Every dollar of AI spend that flows to Microsoft, Google, Salesforce, etc. makes those relationships more consequential.

Pay attention to them accordingly.

Frequently Asked Questions

What percentage of SaaS budget do top vendors typically consume?

Top 10 vendors command 74.2% of average total software spend based on analysis of $18 billion across thousands of companies, a concentration that has remained remarkably stable for three consecutive years from 2023-2025. In absolute dollars, average spend with top 10 suppliers increased 46% from $3.55M in 2023 to $5.21M in 2025, while the long tail of smaller vendors actually shrank as a budget share from 28.3% to 25.8%. This means despite AI tool proliferation creating more line items, spend concentration with major platforms like Microsoft, Google, and Salesforce is intensifying rather than dispersing across more vendors.

Why hasn't AI tool adoption reduced SaaS spend concentration?

Major enterprise platforms captured AI budgets rather than losing wallet share to AI-native challengers by acquiring AI startups, embedding AI features into existing contracts, and raising prices through the AI Tax - 20-37% price increases at renewal compared to historical 3-9% uplifts. Microsoft, Google, and Salesforce aren't threatened by AI-native tools; they're bundling AI capabilities into mandatory packages, forcing SKU migrations, and using AI as justification for aggressive repricing. While AI-native vendors like Cursor grew 4,300% year-over-year and Anthropic 1,900%, they're starting from small bases and remain in the long tail rather than displacing top-10 concentration that has persisted through market correction and transformational technology shifts.

How should I prioritize SaaS budget management across vendors?

Tier your vendor portfolio by spend rather than category, giving top 10 vendors commanding 74% of budget dedicated relationship ownership, quarterly business reviews, board-level renewal visibility, and proactive benchmarking starting 3-6 months before contract expiration. Tier 2 covering next 10-20 vendors receives structured renewal management with defined escalation paths. Everything below gets governed through automated spend alerts and approval thresholds. This prioritization recognizes that 20% discount on $300K HubSpot renewal yields $60K - enough to fund a hire - while the same discount percentage on $15K tool saves only $3K despite requiring comparable negotiation effort and calendar time.

When should I start negotiating renewals for major SaaS vendors?

Initiate renewal conversations at least 3-6 months before contract expiration for top 10 vendors rather than waiting until 30-60 days before opt-out deadlines. Tropic data shows companies engaging six months ahead save 39% more than those waiting until final 30 days, with savings dropping from 39% to 22% at 60 days and 14% at 30 days. Early engagement enables competitive evaluation, usage audits identifying underutilized seats, market benchmarking establishing realistic targets, and consolidation proposals creating bundle leverage. Time is procurement's most undervalued currency - ;ate engagement eliminates walk-away credibility, competitive pressure, and bandwidth for thorough due diligence on contract terms beyond price.

What is SaaS spend consolidation and when should I pursue it?

SaaS spend consolidation involves mapping feature overlap across top vendors to eliminate redundant capabilities and create bundle leverage for better pricing. If Microsoft, Google, and Salesforce all appear in your top 10 - which they likely do - you almost certainly pay for overlapping capabilities across unified communication, productivity suites, CRM, and marketing automation. Each vendor wants increased wallet share, creating incentive to offer bundle discounts when you bring consolidation proposals. Strategic consolidation differs from cleanup exercises: it's proactive vendor negotiation leverage rather than reactive cost cutting, targeting vendors you're consolidating toward rather than eliminating smaller point solutions arbitrarily.

How do I manage AI-driven price increases from major SaaS vendors?

Establish AI spend guardrails before renewal negotiations begin by documenting which AI features you actually use versus what vendors bundle into contracts, establishing ROI thresholds tied to measurable business outcomes, and treating AI pricing as negotiation variable rather than fixed cost. Major vendors apply 20-37% AI Tax at renewal through forced SKU migrations, credit-based pricing obfuscation, and mandatory AI packages. Counter by requesting legacy pricing explicitly, demanding credit consumption transparency with hard caps, separating core product from experimental AI features with different term lengths, and building mid-term review rights if AI consumption exceeds forecasts enabling renegotiation before budget spirals.

What is the long tail in SaaS budgeting and should I ignore it?

The long tail represents smaller vendors outside your top 10, comprising approximately 26% of software spend after recent consolidation from 28% in 2024. Don't ignore it - AI-native tools showing fastest growth like Cursor (4,300% YoY) and Anthropic (1,900% YoY) started in the tail before graduating to strategic importance. Instead, define graduation criteria: at what spend threshold does a vendor move from ad hoc to managed procurement workflows, who owns strategic relationships once tools scale, and what approval processes govern transition from experimentation to dependency. Without clear criteria, tail vendors drift upward in spend without appropriate oversight, turning $20K pilots into $120K dependencies lacking formal playbooks.

Related blogs

Drive savings and efficiency at any stage

Discover why hundreds of companies choose Tropic to gain visibility and control of their spend.