Tropic Intelligence Hub

Where technology becomes a buyer's market

Real-time supplier intelligence, pricing trends, and negotiation insights powered by $21B+ in spend under management. Continuously updated by Tropic's expert team.

Heading

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Key Changes

Heading

Key Changes

Why This Matters

Budget Exposure

Why This Matters

Action Items

Plan for annual budget allocation for Front contracts to avoid premium charges.

Additional Information

Action Items

Action Items

Software spend grew 6x faster at midmarket and enterprise than at SMBs

Software costs went up across the board YoY in Q1 but the increase isn't evenly distributed. Midmarket and enterprise companies saw average software spend climb roughly 20%, while SMBs held nearly flat at 3.5%.

Software spend grew 6x faster at midmarket and enterprise than at SMBs

That 6x gap tells you who has leverage and who doesn't. SMBs can churn, downgrade, or walk away when prices climb. Larger orgs are locked into multi-year contracts, custom integrations, and seat counts that make pushback harder, and vendors price accordingly. Layer in the AI tax and new "intelligence" tiers that rolled out over the past ear and a 20% increase in average spend per company, isn’t surprising.

What this means for you: For mid-market and enterprise buyers, this is the new baseline. If your software budget didn't grow 20% this year, you're either underinvesting or your vendors haven't gotten to you yet. Finance teams should plan accordingly.

SMBs are cutting traditional SaaS to fund AI

AI-Native spend grew 82% to 127% YoY across every segment, but only SMBs used it as a reason to cut legacy SaaS. Midmarket and enterprise are layering AI on top of an already-growing software stack.

SMBs are cutting traditional SaaS to fund AI

One detail worth flagging: Hybrid SaaS+AI (legacy vendors retrofitting AI features) grew slowest in every segment, which tells you buyers are skeptical of tacked-on AI and willing to pay a premium for purpose-built solutions instead.

What this means for you:

- Midmarket and enterprise: Your stack isn't shrinking, it's stacking. Be ready to defend every layer's presence at renewal, not just its price.

- SMB: You have real leverage on traditional SaaS. Bring substitution alternatives to renewals and be ready to walk.

- AI-Native tools: Expect minimal pricing flexibility. Negotiate price caps, usage guardrails, and contract length, not discount percentage.

- Hybrid SaaS+AI: Push on what you're actually paying for real AI capability versus legacy seats. Slow category growth means more flexibility than vendors let on.

Buyers beat the AI price surge by cutting uplifts by 50%

Typical SaaS renewals see single-digit price hikes, but AI vendors are pushing aggressive 20-37% uplifts. Using Tropic's proprietary negotiation tactics, buyers are slashing those AI premiums by over half.

Buyers beat the AI price surge by cutting uplifts by 50%

Insights: Vendors know there continues to be a measurement gap between AI Features and their cost, but the expense of producing AI and the existential promise of what is almost possible, means these uplifts aren’t going anywhere.

What this means for you: Before your next renewal, demand vendor-provided ROI evidence tied to your specific usage, not a case study, your data. If they can't produce it, that's your leverage. Start the conversation 6+ months early, request legacy pricing explicitly, and don't accept a premium you can't validate. Tropic's benchmarking data tells you what comparable companies are actually paying, so you know exactly what you're negotiating toward.

Buyers shift from expansion to replacement as legacy SaaS shrinks

With Net Dollar Retention for traditional software slipping below the critical 100% threshold, the market shift is undeniable. Companies are aggressively cutting bloated legacy contracts to fund new, high-efficiency AI solutions. The question facing every legacy SaaS vendor right now is whether they can build or acquire their way to the AI execution layer before their customers start looking for alternatives.

Buyers shift from expansion to replacement as legacy SaaS shrinks

Insights: Two forces are driving the pressure on legacy vendors. Consumption-based AI pricing is competing directly for the same dollars that previously funded SaaS renewals. And with headcount growth stalled at many organizations, the seat-expansion model that powered SaaS revenue for a decade is running out of runway. Customers aren't just slowing expansion, they're actively cutting.

This is phase one: expansion erosion. Phase two is gross retention, when buyers stop expanding and start replacing. The question facing every legacy SaaS vendor is whether they can build or acquire their way to an AI execution layer before that happens.

What this means for you: Primarily SaaS vendors under pressure are more motivated to negotiate than they've been in years, come to the table with competitive alternatives and usage data. For AI-Native vendors, discounts are unlikely; focus on locking in price caps and uplift protection before your own consumption scales.

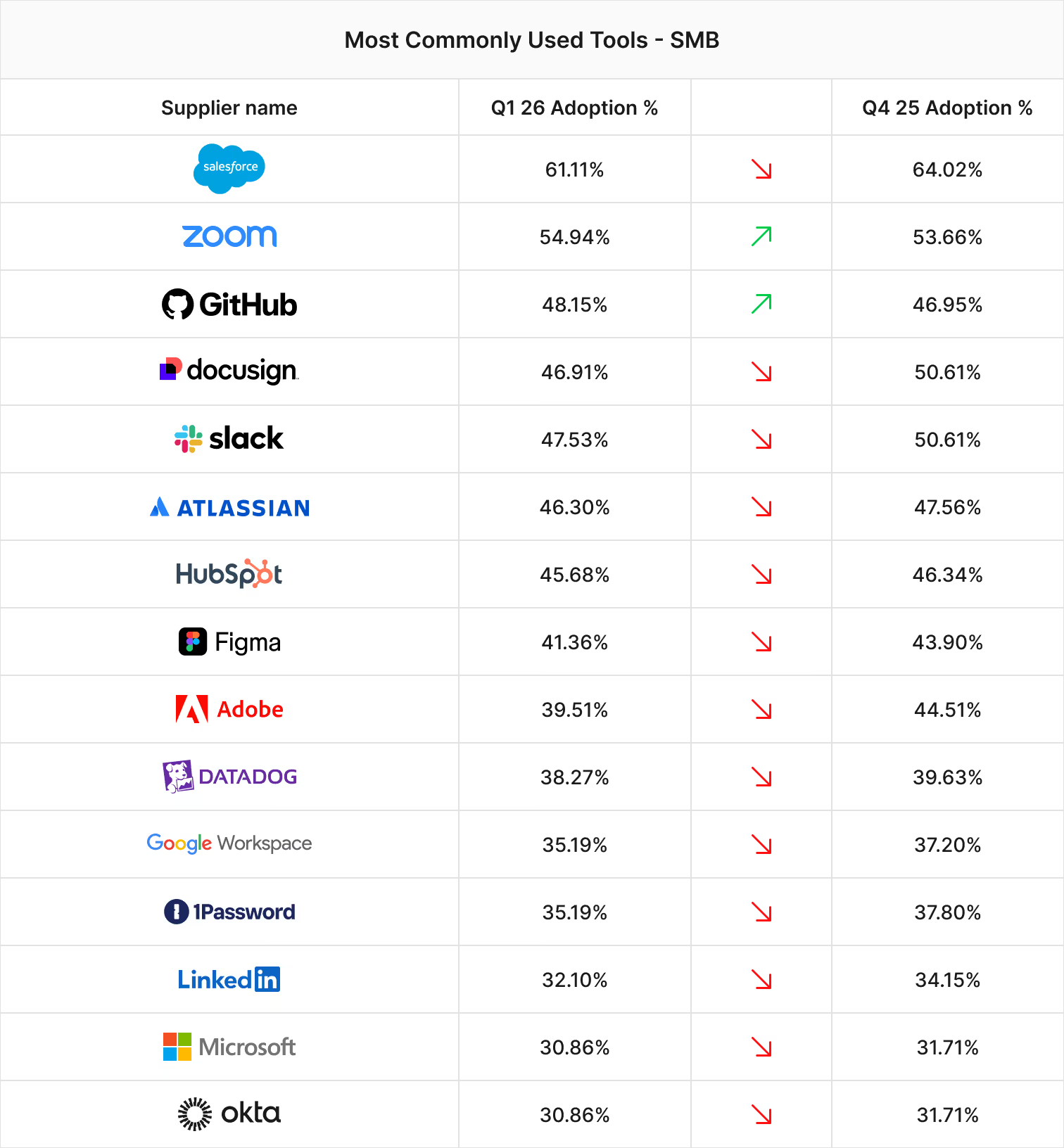

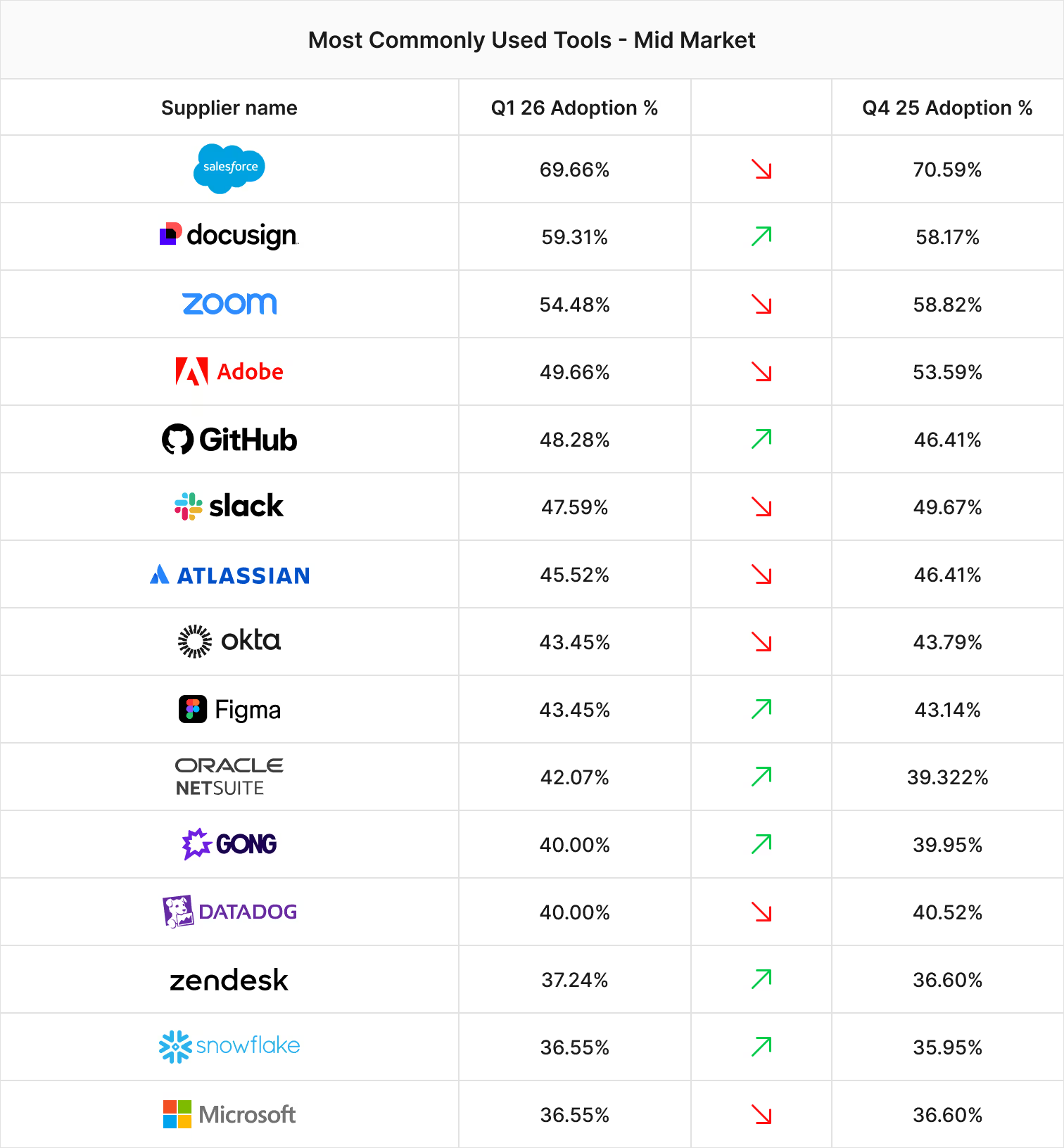

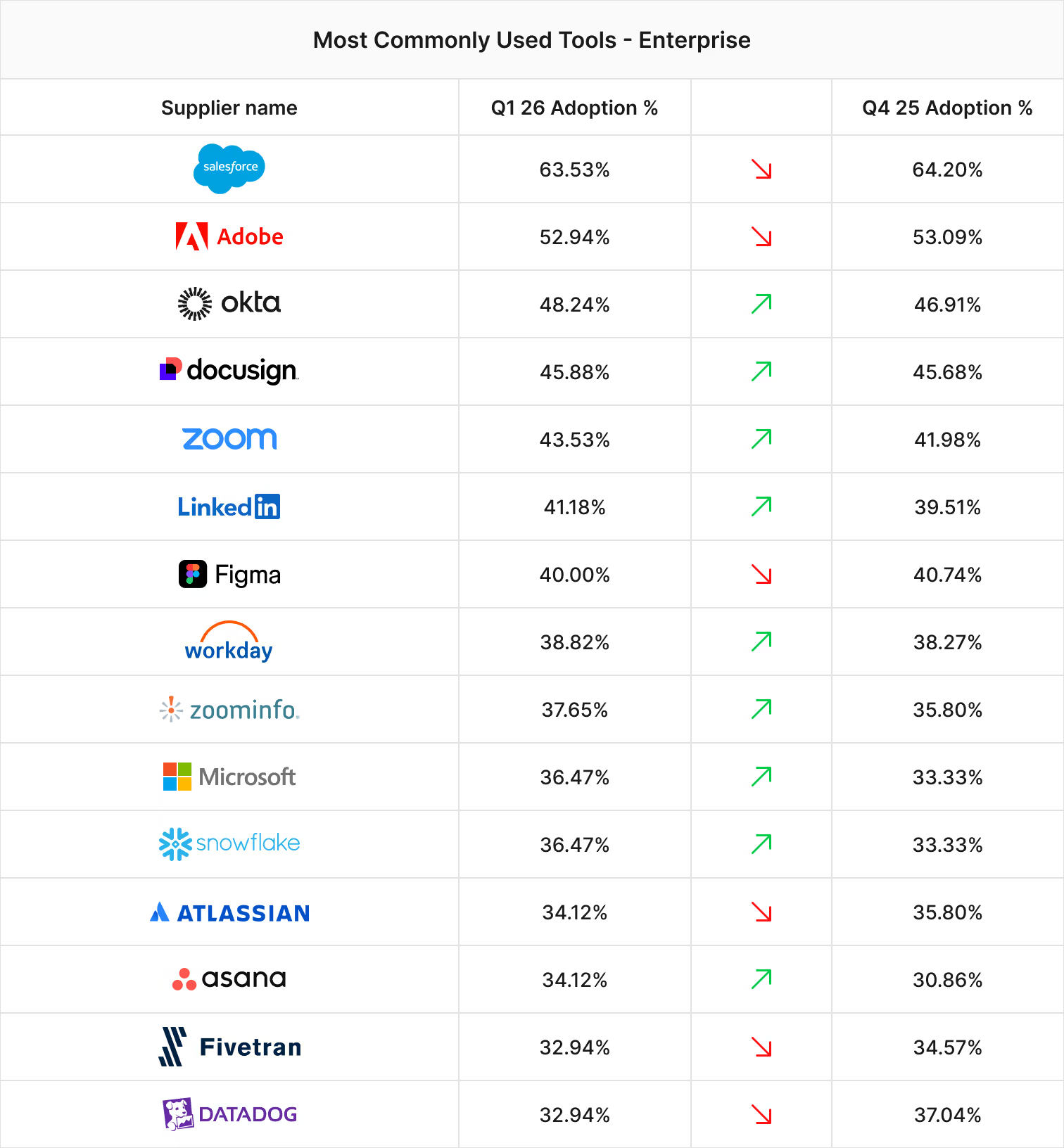

SMBs are starting to prune their tech stack while mid-market and enterprise are swapping

The top of the adoption list (Salesforce, Adobe, Zoom, DocuSign) looks familiar in every segment, but the quarter-over-quarter movement varies by size.

Average SaaS Spend Surges over 50% YoY

SMBs lost adoption on nearly every tool in the top 15. Midmarket is trading collaboration tools out for revenue and finance platforms, with Gong, NetSuite, and GitHub gaining while Zoom and Adobe lost share. Enterprise is more mixed: Microsoft, Snowflake, and Asana gained ground while Datadog dropped 4pp.

What this means for you:

- SMB: Adoption is declining across nearly your entire top 15. Bring substitution alternatives to renewals and ask vendors directly about retention rates for companies your size.

- Midmarket: Collaboration tools are losing to bundled alternatives. If you're paying full price for Slack, Zoom, or Adobe, the consolidation argument is half made for you.

- Enterprise: Tools gaining share (Microsoft, Snowflake, Asana) won't budge on price. Negotiate caps, contract length, and seat commitments instead.

- Watch: Datadog's enterprise drop. If it holds next quarter, observability vendors will be more open to negotiation.

Majority of the fastest growing suppliers charge by consumption

Anthropic tops every list, joined by names like Clay, n8n, Cursor, and Databricks. These vendors price on consumption, not headcount, and that shift breaks the way finance and procurement have budgeted software spend for decades.

Majority of the fastest growing suppliers charge by consumption

Consumption models themselves work. The problem is that the moment a marketing team hits its Clay credit limit mid-campaign, the CFO has two choices: approve more spend or stall the work. There's only one real answer, and it's not the one your annual budget assumed.

What this means for you:

- You can't forecast tech spend with headcount anymore. FP&A, procurement, and engineering already figured this out with AWS, GCP, and Azure. Every functional area needs that same muscle now.

- Build cross-functional accountability before the stack outruns the plan. That means negotiated caps, tiered pricing structures, and real-time usage visibility from day one.

- When evaluating new vendors, ask directly: is this seats or consumption? If consumption, who owns visibility into usage, and what triggers a budget conversation?

- The companies building this muscle now will have a real cost and speed advantage. The ones who wait will spend a lot of board meetings explaining why they're over budget.

Where there's real pricing spread and where you're wasting time negotiating

Price variability tells you where negotiation effort actually matters. The spread between what companies pay for the same tool can be dramatic, or almost nonexistent.The chart below helps understand this volatility. Bars represent the middle 50% of change (25th to 75th percentile), with percentages labeled at each end.

Where there's real pricing spread and where you're wasting time negotiating

What drives variability? Generally, it's a combination of competitive pressure in the category, sales team discretion, contract term length, and how aggressively the vendor is pursuing market share. High-variability vendors are often ones facing meaningful competition or undergoing pricing model transitions.

What this means for you: Understanding price variability can help exponentially when you're negotiating and helps you prioritize negotiation effort on high-variability suppliers. For low-variability suppliers like Figma and Articulate, don't burn cycles trying to move price. Focus instead on terms: payment timing, auto-renewal clauses, and user addition rates.

Use variability data to set realistic internal expectations. Telling stakeholders "we should get 30% off Datadog" sets everyone up for disappointment.

Annual contracts still dominate but their share slipped

The majority of new software contracts where AI is present are still 12 months or less, but that share dropped nearly YoY. Almost all of the shift went into the 13-24 month bucket.

Annual contracts still dominate but their share slipped

What this means for you:

- Annual contracts are still the most common starting point, but 2-year asks seem to be increasing. Be ready for that conversation at renewal.

- If you do agree to a longer term, treat it as a concession worth trading for. Push for price caps, ramp pricing, or termination rights in exchange.

- Multi-year deals (25+ months) remain rare. If a vendor is pushing one, the burden is on them to justify what you get in return.

Traditional SaaS is driving the shift to longer contracts while AI-Native is staying short

The extension trend is almost entirely a SaaS story. Primarily SaaS short-term deals dropped 4.9pp and 13-24 month deals jumped 2.7pp. Hybrid bucket distributions barely moved. AI-Native contracts are still nearly three-quarters short-term

Traditional SaaS is driving the shift to longer contracts while AI-Native is staying short

What this means for you:

- Primarily SaaS: Vendors are actively pushing for longer commitments. That's a defensive play to lock you in before AI alternatives mature. Trade the longer term for stronger pricing or termination rights.

- AI-Native: Short terms are the standard. Don't sign multi-year unless the discount is dramatic. Annual deals preserve your option to swap as the category evolves.

- Hybrid SaaS+AI: Contract length is steady, so there's no clear market signal either way. Negotiate based on individual vendor leverage rather than category trend.

Data insight: Is AI taking up as much share of spend as you think?

POV: $100K saved is more valuable than a $100K new deal?

Guide: How to manage (and reduce) your AI costs

Taking the BS out of SaaS Buying

Expert-led video series on navigating the modern software market

.png)

.jpg)

Finance and Procurement Toolkits

Toolkits for teams navigating the new rules of software pricing in the AI era.

The AI Pricing Playbook

AI vendors are rewriting the rules on pricing. Get free templates to review AI contracts, decode vendor tactics, and forecast AI spend before your next renewal.

Find the Money You Didn't Know You Were Losing

Free templates to surface shadow spend, collect stakeholder data before renewals, and consolidate your SaaS stack. Built for mid-market procurement teams.

Stop Overpaying for Software

Download free templates to negotiate better SaaS contracts — vendor email scripts, 10 questions to ask before signing, and a spend snapshot spreadsheet. Built for lean finance teams.

In Case You Missed It

Key intelligence worth revisiting