The Spend Table is a newsletter and podcast where every conversation could save you money. Subscribe to the newsletter here and watch on YouTube for the latest thoughts from Justin Etkin, Michael Shields, and Russell Lester.

You've seen the headlines: "SaaSpocalypse." "FOBO investing." Billions wiped from software stocks in a matter of weeks. And, while some companies are seeing a little bounce back, the market is continuing to change.

When David Campbell and Justin Etkin started Tropic in 2019, the software landscape was straightforward. Companies were flush with capital, buying every best-in-breed solution, and the SaaS model was considered untouchable. Sticky products, predictable revenue, seat-based growth that basically printed money.

Fast forward to now, and serious questions are being asked about the resilience of that model. Take your average mid-market technology buyer. Legacy SaaS is deeply embedded in their operations, structural dependencies, integrations, workflows built on top of tools they've used for years. But they're also watching AI providers promise better outcomes at lower costs, and the budget is following.

That tension is being felt everywhere. And if you're a CFO or procurement leader managing software buying and renewals right now, you're sitting at the center of it.

Today we're unpacking what's actually happening, and what you should do about it.

What's Actually Happening to SaaS

The short version: SaaS companies are getting hammered in the markets, and the reason matters for how you negotiate your next renewal.

For years, the SaaS growth engine had two fuel sources:

- Seat expansion (more employees = more licenses)

- Price increases

The first fuel source has basically stopped working. Headcount growth at most mid-market companies is flat. Nobody is adding 50 seats of Salesforce right now.

So what do software vendors do when they can't grow through seats? They reach for the other lever: packaging and renewal uplifts. What that looks like in practice is something Justin describes as the AI Tax:

"If we can't rely on utilization to drive growth, we have to look at packaging — 15, 20% off-list type uplifts to compensate for the growth they historically expected from seats."

That's the AI tax. That's one of the reasons your renewal quote looks nothing like last year's.

The AI Tax: How to Spot It Before It Hits Your Budget

The AI tax isn't always labeled as such. Here's how it actually shows up in renewal conversations:

- The Repackaging Move: Your vendor "retires" your current tier and introduces a new one — Enterprise Plus, Advanced Pro, whatever, that includes AI features you didn't ask for and might not use. The price increase isn't 5% or 7%. It's 30% and40% And it's framed as a product upgrade, not a price hike.

- The Forced Bundle: Features you previously purchased à la carte are suddenly only available in a higher-cost tier that includes AI add-ons. You're not comparing apples to apples anymore, which is exactly the point.

- The Consumption Shift: A vendor moving toward usage-based pricing on AI features with no clear ceiling. You sign a renewal at a familiar annual number, and then AI usage starts accruing separately.

Michael has watched this play out firsthand:

"A few years ago we were seeing bigger uplifts than normal, but lately it's been trickier to identify, they're repackaging features with AI and bundling things together."

🎯 Your move: Before any renewal conversation, pull your utilization data and map it to what you're actually being asked to pay for. If a vendor can't show you a clear breakdown of what you're getting for the AI premium, that's your negotiating leverage.

And keep your options open, maintaining competitive alternatives isn't just a negotiation tactic right now, it's a strategic posture. In a market where vendors are restructuring pricing and your stack is being disrupted anyway, optionality is your friend on every major renewal.

AI Sprawl 1.0: The Pattern You've Already Lived Through — Again

You've seen this movie before. It may not feel like it. AI is shiny and awe-inspiring, and is genuinely transforming how you do everything. But, so did the internet. So did SaaS.

Think back to 2019–2022. Low unit costs, easy procurement bypass, shadow purchasing, one-click sign-ups, and then a reckoning when someone finally pulled the spend report. Tech stacks exploded because capital was flowing, the tools were cheap, and nobody was watching closely enough.

AI tools follow the same pattern, but faster. One team member signs up for an AI writing tool. They invite two colleagues. Those colleagues invite their reports. Within a quarter, you have 40 seats, three overlapping contracts, and nobody knows who approved what.

Russell put it plainly saying:

"This is tech stack sprawl 2.0. Unless they're paying attention, they're going to quickly find several months from now they have many more tools than they realized, because they're buying little bites of these AI tools that are pretty cheap in the beginning."

The difference this time: the initial price point is lower, which makes it easier to slip through procurement review, and the expansion dynamics are murkier because many AI tools price on consumption, not seats. That budget toward AI is moving fast, and a lot of it is moving without proper controls.

Where Are Budgets Coming From?

There's an impossible position boards are putting procurement and finance in right now. As Russell said:

"This is tech stack sprawl 2.0. Unless they're paying attention, they're going to quickly find several months from now they have many more tools than they realized, because they're buying little bites of these AI tools that are pretty cheap in the beginning."

There is no new pot of money called AI. And, the budget for AI investment isn't just coming from the software line. It's coming from the people side of the P&L too. Engineering and product resources that previously went toward bug fixes and feature work are increasingly being redirected toward internal AI build ambitions.

That interplay between the technology budget and the headcount budget is something CFOs need to be tracking together, not separately, because they're no longer separate decisions.

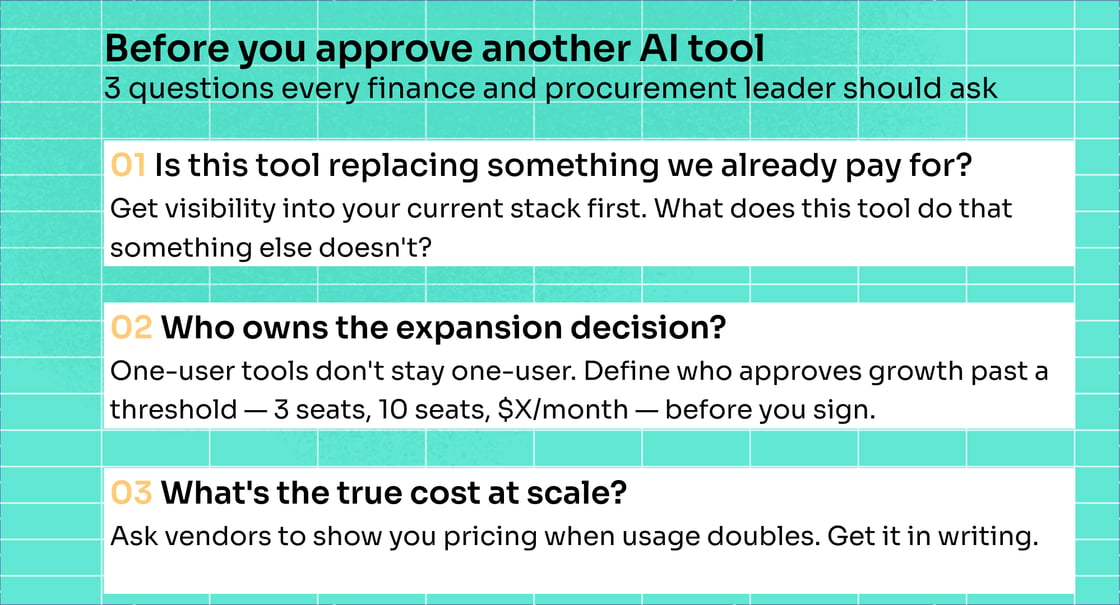

🎯 This is also where procurement earns its seat at the table or loses it. You need to be able to answer: which tools do we cut to fund the AI we actually need?

That requires two things most teams don't have today:

- Complete visibility into current utilization

- A framework for evaluating new AI tools against existing spend

The Build vs. Buy Question Is Now a Procurement Question

This one deserves its own newsletter, and it'll get one soon. But it can't go unaddressed here.

Companies are increasingly asking, mid-procurement process, "why can't we just build this with the AI we already have?" According to recent data, 35% of enterprises have already replaced at least one SaaS tool with a custom build, and 78% expect to build more internal tools in 2026.

That used to be an IT or product engineering conversation. Now it's showing up in purchase request reviews. Whether or not building internally is the right answer, this is now a question procurement has to be equipped to evaluate.

And, Michael's take is worth sitting with: this isn't a pro-build or pro-buy question. It's a total cost of ownership question. Building can move fast. It also requires constant maintenance, competes for technical resources, and often lacks the roadmap progression that a dedicated vendor provides. Things like Claude Code are making build more a reality, but there is still A LOT to consider.

The better question isn't "why buy when I can build?" It's "what are the total costs of buying versus building over a defined period of time?" If you can't speak to the build-vs-buy calculus when a stakeholder raises it, someone else will make that call for you.

What You Should Do Today

🎯 If you're a CFO: Don't wait for renewals to tell you what's happening to your tech spend and stack.

- Pull a spend report filtered to tools under $10K/year — that's where AI sprawl hides

- Flag every renewal in the next 90 days and note whether AI uplifts are expected

- Ask your procurement lead: do we have utilization data for each of these tools?

- Map your top vendors' pricing changes YoY — if they've repackaged, find out what changed

- Connect the software budget conversation to the headcount conversation before your next board update

🎯 If you're in procurement: This is your moment. As Michael put it:

"Procurement's always been asking for that seat at the table. Here is a tremendous opportunity, this will be a need that basically every single company will encounter."

But you can't capture it by staying in reactive mode. Instead:

- Audit new AI tool requests from the last 60 days — how many overlap with existing tools?

- Set expansion thresholds now, before the next request hits your desk

- For every upcoming renewal, request vendor utilization data before the first call

- Build your competitive alternatives list for your top 10 vendors — optionality is your leverage

- Start your next renewal conversation at least 90 days out — timing is your single biggest savings lever

🎯 For both: Get ahead of the AI tax conversation before your vendors do. Going into a renewal cold, without benchmark data, without utilization data, without competitive context — is exactly the position these vendors are counting on.

The Numbers to Keep Handy

.png)

- 94% — Year-over-year spend growth on AI-native tools among mid-market companies

- 8% — Year-over-year spend growth on legacy enterprise SaaS (down from the 10–20% clip of prior years)

- 15–40% — The range of AI-driven renewal uplifts showing up in real negotiations today

And from the broader market: the “SaaSpocalypse” has erased significant value from public SaaS stocks since early February 2026. Vendors under margin pressure find ways to recover it, and renewal season is the most reliable place to do that.

Where This Leaves You

We don’t think we’re in a SaaSpocalypse. Salesforce isn't going anywhere. ServiceNow isn't going anywhere. But the business model pressures these companies face are very real, and the clearest path for them to address those pressures runs directly through your renewal contract.

The procurement and finance leaders who understand this dynamic, who have the data to challenge it, and who are proactive rather than reactive, are going to come out of the next 12 months with stronger vendor relationships and leaner, smarter tech stacks.

Drive savings and efficiency at any stage

Discover why hundreds of companies choose Tropic to gain visibility and control of their spend.